Atrium

Accéder à notre plateforme en ligne pour gérer votre police d’assurance-crédit.

Belgique

Belgique

Allemagne

Allemagne

Australie

Australie

Autriche

Belgique

Autriche

Belgique

Brazil

Brazil

Bulgarie

Bulgarie

Canada

Canada

Chine

Chine

Danemark

Danemark

Émirats arabes unis

Émirats arabes unis

États-Unis

États-Unis

Finlande

Finlande

France

France

Grèce

Grèce

Hong Kong

Hong Kong

Hongrie

Hongrie

Inde

Inde

Irlande

Irlande

Italie

Italie

Japon

Japon

Lituanie

Lituanie

Mexique

Mexique

Norvège

Norvège

Nouvelle-Zélande

Nouvelle-Zélande

Pays-Bas

Pays-Bas

Pologne

Pologne

Portugal

Portugal

République tchèque

République tchèque

Roumanie

Roumanie

Royaume-Uni

Royaume-Uni

Singapour

Singapour

Slovaquie

Slovaquie

Slovénie

Slovénie

Spain

Spain

Suède

Suède

Suisse

Suisse

Turquie

Turquie

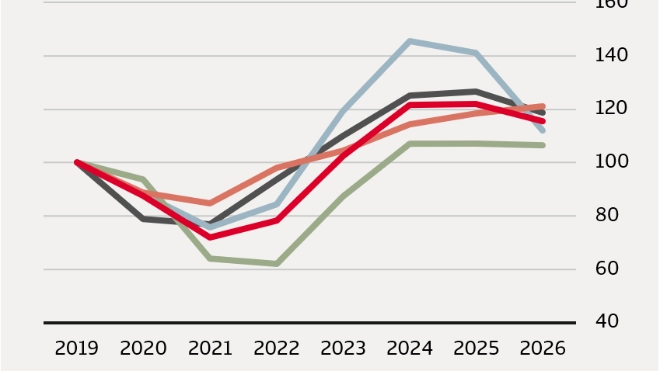

Selon les dernières prévisions d'Atradius en matière d'insolvabilité, le nombre de faillites devrait se stabiliser en 2025 et légèrement diminuer en 2026. Cela indique un retour à une dynamique commerciale plus normale après les pressions intenses de ces dernières années, telles que la forte inflation, la hausse des taux d'intérêt et la suppression des mesures de soutien liées à la pandémie.

En 2024, le nombre de faillites dans le monde a augmenté de 19 %, avec une hausse significative dans presque tous les marchés étudiés. Les entreprises ont dû faire face à une hausse des coûts d'exploitation, à un accès limité au crédit et à des dettes persistantes liées aux mesures de soutien gouvernementales. Dans des pays comme l'Australie, l'Irlande et le Canada, la fin des mesures liées à la pandémie a contribué à la flambée des faillites d'entreprises. Dans d'autres pays, tels que l'Allemagne et le Japon, les pressions économiques structurelles et les faibles performances industrielles ont accentué la pression.

Pour l'avenir, on s'attend à ce que 2025 marque un tournant. Environ la moitié des 29 pays couverts par le rapport devraient voir le nombre de faillites diminuer, tandis que d'autres pays continueront à faire face à des difficultés. À l'échelle mondiale, le nombre total de faillites devrait rester stable en 2025 par rapport à l'année précédente, avant de baisser d'environ 5 % en 2026.

Les banques centrales ont commencé à assouplir leur politique monétaire en réponse au ralentissement de l'inflation, ce qui devrait progressivement réduire les coûts de financement et soutenir la reprise des entreprises. La Banque centrale européenne a commencé à baisser ses taux d'intérêt à la mi-2024, suivie par la Réserve fédérale américaine plus tard dans l'année. Ces changements devraient alléger quelque peu la pression financière sur les entreprises, même si les effets positifs ne se feront sentir qu'à plus long terme.

Malgré l'amélioration du climat de crédit, l'accès au financement reste quelque peu limité en raison de la persistance de l'incertitude économique. Les enquêtes sur l'octroi de crédits par les banques indiquent une attitude prudente des institutions financières, en particulier aux États-Unis et dans la zone euro, ce qui pourrait encore freiner la croissance des entreprises et les investissements à court terme.

L'une des principales incertitudes réside dans l'escalade des tensions commerciales mondiales. Dans notre scénario de base, nous partons du principe que l'impact des nouveaux droits de douane sur le nombre de faillites sera modéré. Toutefois, dans un scénario pessimiste prévoyant une guerre commerciale totale, le nombre de faillites dans le monde pourrait à nouveau augmenter, de 6 % en 2025 et de 5 % en 2026, en raison d'un ralentissement de la croissance, en particulier dans les économies ouvertes telles que les Pays-Bas et les principaux pays exportateurs d'Asie.

Cet aperçu ne présente que quelques-unes des principales conclusions. Téléchargez ci-dessous le rapport complet Insolvency Forecast 2025-2026 pour obtenir un aperçu détaillé des prévisions par pays, des tendances économiques et des analyses de scénarios.