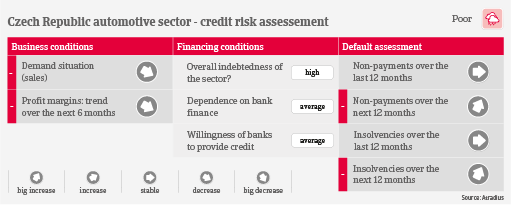

A sharp increase in automotive insolvencies is expected

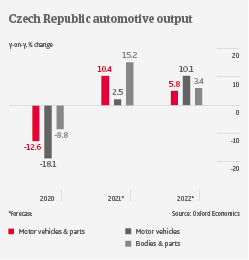

After contracting 18% in 2020, Czech motor vehicles output is forecast to rebound by only 2.5% in 2021, as car manufacturers have been forced to curb production due to shortage of semiconductors and other components. Since Q2 of 2021 turnover has started to decline for Original Equipment Manufacturers (OEMs) and suppliers alike, expected to decrease by about 30%-40% this year. Profit margins of businesses have started to deteriorate due to higher costs for raw materials, energy and labour, while increased interest rates weigh on highly leveraged businesses. At the same time, another major surge of coronavirus cases and subsequent restrictions remain downside risks.

Payments in the industry take 60 days on average, and the number of non-payments and insolvencies has been low so far, due to government support and the rebound seen in early 2021. Currently most businesses still hold enough cash to meet their liabilities, but their cash flow will get under strain in the coming months. Both payment delays and insolvencies are expected to increase by up to 30% in the coming twelve months, as government support will be phased out, and ongoing issues (semiconductor shortage, high input prices) will persist into 2022. Larger producers are expected to remain resilient, with many of them being part of an international group. However, the credit risk of smaller and mid-sized suppliers will increase, in particular of businesses which are highly leveraged and/or have high external financing needs.

Our underwriting stance is generally cautious for the industry. All businesses are assessed on an individual basis, with respect to their financial position and performance outlook. Many suppliers are facing the need for additional investments in order to cope with the shift from combustion engines to e-mobility. Not all of them will be able to cope with this challenge, and some Tier 2 & 3 suppliers will be forced to leave the market in the coming 2-3 years. In the car dealing segment the situation is currently stable, as many businesses are able to compensate lower sales volumes with higher prices.